We explore market trends, search engine optimization and artificial intelligence strategies, and the essential technical components for professional development.

However, there is a critical gap that most financial institutions fail to close. They have functional, sometimes even visually appealing, quote tools, but these remain passive, relying entirely on user initiative to move through the sales funnel. The visitor takes a guess, gets a number, and leaves, taking the information with them without leaving an identifiable trace.

This second part addresses precisely that gap. We'll analyze how to transform your price estimator from a simple mathematical tool into a strategic asset for lead generation, nurturing, and conversion. We'll examine data architectures that enable real-time personalization, the points of friction that kill conversions, and the integrations that turn an anonymous simulation into an identified and actionable business opportunity.

The goal is clear: that every visit to your price quote tool, regardless of whether the user completes a formal request, generates measurable and sustainable business value for your organization.

This scenario is all too common in Latin American fintech. A prospect arrives at the price quote tool after an organic search or a paid campaign. They enter amounts and terms, explore different scenarios for five, ten, or fifteen minutes. Finally, they get a detailed projection and leave the site without providing their name, email, or phone number.

For the financial institution, this behavior represents a total loss of the acquisition investment. There's no way to contact the interested party, understand why they didn't proceed, or retarget them with relevant offers. The potential lead vanishes into digital anonymity.

Industry metrics are revealing. According to consolidated data from multiple institutions, between 60 and 80 percent of users who complete a simulation abandon it without identifying themselves. Of those who remain, many provide false information or secondary email addresses that they never verify. The conversion rate from simulation to formal application rarely exceeds 15 percent in the traditional financial sector.

This massive loss of opportunities is not inevitable. It represents a design flaw in the conversion architecture, not an inherent characteristic of consumer behavior. Users don't abandon the process because they're uninterested; they abandon it because the transition from anonymous simulation to identified engagement is designed as an abrupt jump rather than a gradual ramp.

The solution to the anonymous simulation problem lies in reimagining the price quoter as a progressive value exchange system, where each user interaction unlocks additional functionality in exchange for incremental information.

Instead of requiring name, email, and phone number at the beginning, blocking access to the simulation, the progressive conversion model allows full exploration with minimal or no data, and introduces strategic exchange points where the user voluntarily provides information in exchange for tangible value.

The first point of exchange typically occurs after the initial simulation. The user has entered their parameters and receives the basic result: amount, term, monthly payment. At this point, before displaying the detailed breakdown or amortization tables, the system offers: "To save your simulation and receive the complete analysis by email, enter your email address." The perceived value of the detailed breakdown outweighs the psychological cost of providing an email address.

The second point of interaction arises when the user explores multiple scenarios. After comparing three or four configurations, the system suggests: "Would you like our specialist to analyze which option best suits your profile? Schedule a no-obligation fifteen-minute call." Here, the value is personalized advice, and the cost is the time commitment of a call.

The third point of exchange, for users who have returned multiple times, offers notifications: "Rates change frequently. Would you like us to alert you when there's a better option for your profile?" The value is timely information, and the cost is the acceptance of marketing communications.

This architecture recognizes that the value of user information increases with their level of engagement, and designs the flow to capture it at the moment of maximum interest, not at the beginning when distrust is greatest.

Even with the best progressive conversion architecture, certain pain points systematically destroy the lead generation capabilities of a price quote tool. Identifying and eliminating these points is a priority for any serious development.

The first point of friction is slow calculation speed. Users expect instant results; every second of waiting after entering parameters exponentially increases the abandonment rate. Complex financial operations must be optimized to run in milliseconds, using pre-calculation, intelligent caching, or asynchronous processing that displays preliminary results while the final results are being refined.

The second point of friction is the complexity of data entry. Requesting information that the user doesn't have readily available, such as a spouse's exact income or details of existing debts, disrupts the flow and leads to abandonment. Effective loan calculators use intelligent estimations, sliding ranges, and conditional logic that only requests details when they are strictly necessary for the calculation.

The third point of contention is the lack of transparency in the methodology. When users don't understand how the displayed result was obtained, mistrust hinders progress. Each figure should be broken down to show its origin: this installment includes principal, interest at this rate, mandatory insurance of this amount, and a commission of this percentage. Transparency builds trust, which facilitates conversion.

The fourth point of friction is the lack of comparative context. An isolated number, such as a monthly fee of five hundred dollars, is meaningless. Is it high or low? How does it compare to other options on the market? Lead-generating quote tools include contextual benchmarks: this fee represents twenty percent of your estimated income, it's within the healthy range recommended by financial experts, and it's competitive compared to the market average for this profile.

The fifth and most critical point of friction is the abrupt transition to a formal request. The leap from "simulating" to "requesting" often involves a change in interface, lengthy new forms, and a perceived legal obligation. High-converting quote providers design this transition as a natural continuation, maintaining the context of the simulation and requesting only the additional information strictly necessary to formalize the request.

-(1)-0406191938.png)

This comparison illustrates why investing in the development of advanced quoting tools generates higher returns than simply acquiring traffic for basic tools.

Is your pricing tool capturing the sixty percent of leads you're missing? At Presticorp, we develop progressive pricing tools that transform anonymous visitors into identified business opportunities. Schedule an audit of your current tool and receive a conversion diagnosis with no obligation.

-0406192946.png)

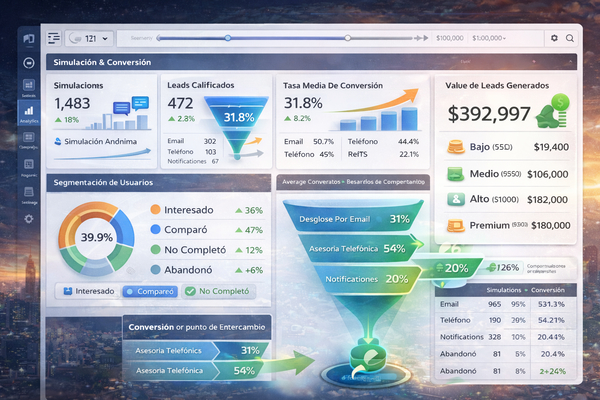

Progressive conversion architecture for a financial price quote tool, showing value exchange points where the user voluntarily provides data in exchange for incremental benefits. Source: Presticorp, 2026 development methodology.

A price quoting tool, however sophisticated its conversion architecture, remains ineffective if it doesn't directly feed into sales management systems. CRM integration represents the bridge between the digital experience and sales action.

Basic integration synchronizes the captured data: name, contact information, simulation parameters, and interaction time. This allows an advisor to contact the prospect with complete context, knowing exactly which scenarios they explored, how much time they spent, and what potential pain points the system identified.

The intermediate integration adds automatic lead scoring. Based on user behavior in the quote generator, the system assigns scores: a user who simulated five different scenarios, returned three times in a week, and requested a detailed breakdown receives a high purchase intent score. A user who simulated once with minimal parameters and immediately abandoned the process receives a low score. The CRM prioritizes sales contacts accordingly.

Advanced integration enables automated nurturing. Leads not ready for a phone call receive a sequence of personalized emails based on their specific behavior: education about the type of product they simulated, market comparisons, testimonials from similar customers, and eventually a new invitation to chat when their engagement score indicates readiness.

This integration requires robust APIs, careful field mapping, and data governance that respects privacy regulations. The technical investment is significant, but the return in business efficiency and conversion rate more than justifies it.

Discover the true potential of your quoting tool. Try our web development pricing tool and receive a detailed estimate of investment, timelines, and expected return for your financial quoting project in minutes . No sales calls, no obligation, just clear numbers.

After developing and implementing price estimators for financial institutions of various sizes and specialties, I want to share observations that rarely appear in technical specifications but determine the success or failure of these projects.

First suggestion: visual design matters less than you think, and response time matters more than you imagine. We've seen aesthetically sophisticated quote generators fail due to load times exceeding three seconds, while visually simple ones generate massive leads because they respond instantly. Invest in performance optimization before complex animations.

Second suggestion: users lie, but their behavior doesn't. The data users enter into quote generators is often optimistic or incomplete. But their behavior—what scenarios they explore, how often they return, what breakdowns they request—reveals their true situation. Design your system to capture and analyze behavior, not just to process declarative input.

Third suggestion: The best CRM integration is the one the sales team actually uses. We've seen technically perfect integrations ignored by advisors who prefer their personal spreadsheets. Involve the sales team from the design stage, adapt the workflow to their existing practices, and provide ongoing training. Technology without adoption is an expense, not an investment.

Fourth suggestion: Quoters have a limited lifespan without evolution. Rates change, products are updated, and regulations evolve. A quoter that isn't actively maintained becomes a reputational liability when it displays outdated information. Budget for ongoing maintenance, not just initial development.

Fifth suggestion: measure the lifetime value of the lead generated, not just the immediate conversion rate. Some of our clients have discovered that leads who didn't apply immediately, but received proper nurturing, became higher-value customers within six months. The quote is the beginning of a relationship, not just a transaction.

Online price quoting tools have completed their evolution from utility tools to strategic business generation assets. The difference between a quoting tool that simply calculates and one that converts lies in the progressive capture architecture, the systematic elimination of friction points, and intelligent integration with business processes.

For financial institutions competing in saturated markets, where product differentiation is minimal and competition for customer attention is fierce, a price comparison tool represents a defensible competitive advantage. It is not easy to replicate: it requires investment in development, a deep understanding of user behavior, and alignment between technology and business operations.

The question for leaders of financial institutions is not whether they can afford to develop an advanced quoting tool. The question is whether they can afford to continue using tools that capture less than 15 percent of the value of the interactions they generate, while more sophisticated competitors capture 40 percent or more.

The Latin American fintech market is currently consolidating, and customer acquisition efficiency will determine the winners. A well-designed and implemented price quote tool is one of the most powerful levers for achieving that efficiency. Want to see how a truly optimized quote tool performs? Access our price quote tool, simulate your financial web development project, and experience firsthand the progressive conversion architecture we describe in this article . Then decide if we'd like to talk.

-

-

-

-

-

-

-

-

-

-

-

-

-

-

McKinsey and Company. Digital Banking in Latin America: The Fintech Revolution. McKinsey Financial Services Practice, 2025.

SalesforceResearch. State of the Connected Customer: Financial Services Edition. Salesforce.com, 2024.

HubSpot. The Ultimate Guide to Lead Generation Forms: Conversion Benchmarks 2025. HubSpot Research, 2025.

ForresterResearch. The Total Economic Impact of Progressive Profiling in B2B Financial Services. Forrester Consulting, 2024.

Gartner. CRM and Customer Experience Strategies for Financial Services. Gartner Customer Service and Support Practice, 2025.

Presticorp Internal Data. Performance Analysis Quotation Tool: 50+ Implementations 2020-2025. Financial Project Database.

Adobe Digital Economy Index. Financial Services Digital Conversion Benchmarks. Adobe Analytics, 2025.

Deloitte Digital. The Future of Financial Services Customer Acquisition: 2026 Outlook. Deloitte Center for Financial Services, 2025.

Si tu proyecto requiere una solución más enfocada, entra directo a la landing ideal para tu negocio y envíanos tu información en el formulario correspondiente.

0 Comentarios